Commissioning engineers don’t materialise because you’ve announced a project. And in Tier-2 markets, they’re not there waiting. That’s the talent reality behind the biggest shift in European Data Center investment right now, and it’s one the capital allocation models rarely price in.

Half of major Data Center REITs are now prioritising Tier-2 cities. The reason is straightforward: the FLAP-D markets, Frankfurt, London, Amsterdam, Paris and Dublin, are running out of room. Grid connection lead times of 2 to 4 years. Land values doubled since 2023. A moratorium in Amsterdam. Frankfurt constrained until 2028.

The capital is moving. Milan, Madrid, Warsaw, Berlin, Manchester, Lisbon, the Nordics, the GCC. The EUDCA projects 176 billion euros in cumulative European Data Center investment between 2026 and 2031. Roughly 270 MW of the 1,000 MW currently being built across European metros is targeted at Tier-2 locations.

The investment thesis has found these markets. What it hasn’t found is a way to staff them.

Why FLAP-D’s Talent Model Doesn’t Travel

FLAP-D markets built their Data Center workforces over 20+ years. Clusters of operators, contractors, OEMs and consultancies created a self-reinforcing ecosystem. Experienced commissioning engineers, MEP designers, BMS specialists and construction leaders concentrated in these hubs because that’s where the work was. Training pathways fed into them. Recruitment agencies built networks there.

Tier-2 markets have none of that.

When a hyperscaler announces a campus build in Zaragoza, or a colocation provider breaks ground near Milan, they’re entering a market where the local construction workforce may be experienced in commercial or industrial build. But Data Center commissioning, high-density power distribution and precision cooling are specialist disciplines. The gap between available local talent and what the programme actually requires is significant.

Every new campus announcement in a Tier-2 market is a region-changing event that can instantly exhaust the local talent pool. Unlike software engineers, these professionals must be physically on site.

Programme Directors tell us this is already their biggest operational risk. “I have the budget, the site, the power allocation. What I don’t have is 15 commissioning engineers willing to relocate to a city they’ve never worked in.”

That’s not a recruitment problem. It’s a programme delivery risk, measured in delayed commissioning, extended contractor cover, missed revenue from uncommissioned capacity, and reputational damage with end clients. And it’s one the site-selection process should have anticipated.

The Recruitment Problem Tier-2 Actually Creates

In FLAP-D, operators compete on brand recognition. Engineers know who Equinix is. They know VIRTUS, NTT, Digital Realty. The employer brand does half the work. A job advertisement in Frankfurt reaches candidates who already understand what the role involves.

In a Tier-2 market, none of that applies. The mission-critical engineering workforce didn’t develop in these markets because the work wasn’t there. Two specific problems compound quickly.

Thin local pools

A Data Center build in Warsaw needs the same calibre of commissioning manager as one in Frankfurt. Warsaw doesn’t have Frankfurt’s ecosystem. International mobilisation, relocation packages, visa processing and compliance all add weeks to already compressed timelines. According to Uptime Institute, 51% of data center operators struggled to find qualified candidates in 2024, with only around 15% of applicants meeting minimum qualifications. In a FLAP-D market, that ratio is at least workable. In Tier-2, it’s a crisis.

Relocation resistance

Experienced engineers with established lives in FLAP-D markets aren’t easily convinced to move for a 2-year programme. The compensation needs to reflect the disruption. The career proposition needs to be genuinely compelling. And the employer brand, which did the heavy lifting in Frankfurt or Dublin, now needs to be actively sold to candidates who’ve never considered the destination market.

There’s also no safety net. In FLAP-D, if a contractor finishes and leaves, you can replace them within the local market. In a Tier-2 city, a single departure can create a programme-critical gap that takes months to fill. The margin for error in workforce planning is thinner. The cost of getting it wrong is measured in delayed commissioning and uncommissioned capacity.

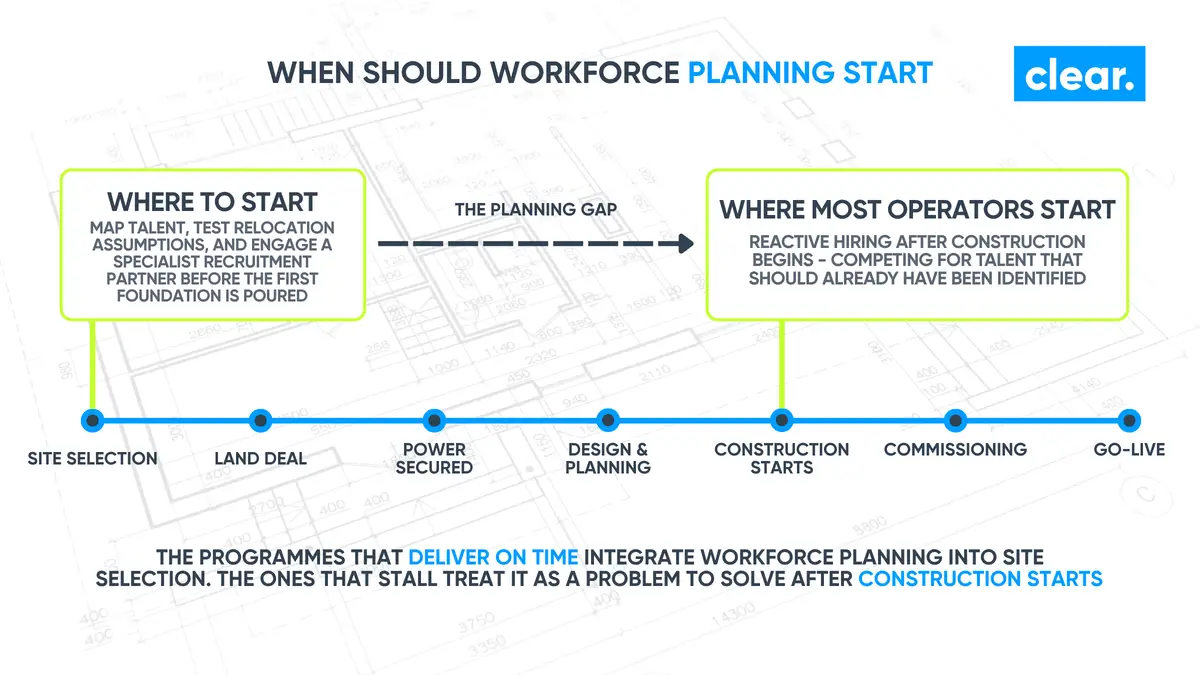

The Site-Selection-to-Staffing Playbook

The developers de-risking Tier-2 expansion aren’t separating site selection from workforce planning. They’re integrating them into a single decision framework. The distinction between the programmes that deliver on time and the ones that stall comes down to four things.

Talent availability as a site-selection variable

Before signing a land deal, the forward-thinking operators are asking: what’s the local engineering workforce profile? How many qualified MEP, commissioning and controls professionals are within commutable distance? What adjacent industries exist that could supply transferable skills?

If the answers are thin, that’s a cost and a risk that belongs in the feasibility model. Not a problem to solve after construction starts.

Early engagement of a specialist recruitment partner

Not at mobilisation. At site selection. Clear operates from London, New York and Dubai, placing engineers across EMEA, North America and the GCC. When a client asks us to assess workforce availability in a Tier-2 market, we can map the local talent landscape, identify adjacent industry sourcing routes, and pressure-test relocation assumptions before a single foundation is poured. That intelligence shapes the programme plan, not just the recruitment plan.

Cross-border mobilisation of proven teams

An engineering director who just delivered a hyperscale programme in Dublin has the credibility to lead one in Milan. A commissioning team that’s completed a build in Virginia can mobilise to the GCC. The challenge is identifying them before their current programme completes, and making the Tier-2 opportunity compelling enough to move for.

That requires a network built across every active programme, not just a database in the destination market. We’ve made 160+ placements for operators and contractors including NTT, VIRTUS, Winthrop and Dornan across multiple countries and programme types. That cross-programme visibility is what makes early identification possible.

Adjacent industry sourcing

This lever becomes more powerful outside FLAP-D. Madrid has a deep pool of electrical and mechanical engineers from its energy sector. Warsaw has technical professionals from manufacturing. The Nordics have power systems engineers from renewables. These are professionals with transferable skills in high-voltage systems, precision controls and complex delivery under regulatory frameworks.

Transitioning them into Data Center roles requires a partner who can explain what mission-critical standards mean and position the career trajectory in a way that resonates. Our 83+ placements across power and cooling OEMs including Anord Mardix and Airedale reflect exactly this kind of adjacent-industry pipeline in practice.

Talent Is the Variable That Separates the Programmes That Deliver

The capital is there. The power is being secured. The sites are being acquired. Every Tier-2 market on the investment shortlist has a land deal, a power allocation, and a build timeline.

What most of them don’t have is a workforce plan that started early enough.

Talent in Tier-2 markets doesn’t show up because you’ve announced a project. It shows up because you planned for it at site selection.

The next decade of European Data Center delivery will be defined by who can execute in markets that didn’t have a Data Center ecosystem 3 years ago. The site-selection-to-staffing playbook isn’t a recruitment strategy bolted on at the end. It’s a programme delivery strategy built in at the beginning.

Clear recruits across Data Center, power and cooling infrastructure from London, New York and Dubai. If your workforce plan hasn’t caught up with your capital plan, talk to our team.

clear-er.com